At 6:42 a.m., Sandra was consuming instant coffee before heading to school when the email arrived on her phone. The subject line said, “Update to your State Pension age.” Thinking it was spam, she nearly swiped it away. The toast in her hand felt a little heavier than it had a minute before when she saw the words “born in March” and “rising in 2026.”

Born in March 1968, she is 58 years old and has been silently counting down the years until she receives her State Pension like a person watching the clock in the final hour of a long shift. In just a few official paragraphs, that clock appears to be moving once more.

What’s the worst? She is by no means alone in this silent shift happening.

State pension age in 2026: the subtle shift that affects birthdays in March

People who were born in the middle to late 1960s are gradually realising that their retirement plans are changing all over the United Kingdom. Not in a big way. Don’t use fireworks. Only with minor technical adjustments to the State Pension age that are communicated through courteous emails and dry letters.

For people born in March, the date of their birthday is going to be more significant than they ever thought. Months of work can be added in a matter of weeks. The finish line may be moved once more by a different year on the birth certificate.

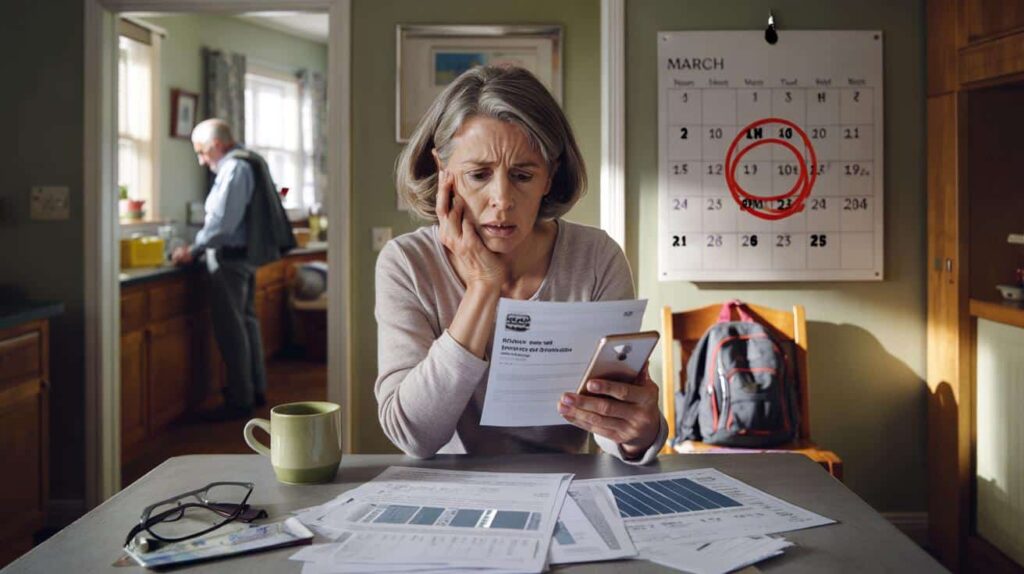

Imagine two former classmates, Lisa (born February 28, 1968) and Karen (born March 3, 1968). For years, they have made jokes about “retiring together exchanging” links about inexpensive flights and campervans. One of them then discovers that the dates don’t match when they look up their State Pension forecast online.

One may make a claim sooner. Due to the State Pension ages being raised to 67 and then 68, the other must wait a little while longer.

A 20-year shared dream is subtly destroyed by a few dates in a government schedule.

In summary, the government has already passed legislation raising the State Pension age to 67 between 2026 and 2028, and it is currently monitoring the rate of increase after that. People who were born in particular years, particularly those who were born in March, are directly affected by those changes.

Reasons are frequently attributed to an ageing population living longer, and declining public finances. On paper, the reasoning makes sense. In reality, it falls on bodies that may already be exhausted from decades of manual labour shift work, or caregiving duties.

- This one habit prevents clutter without constant work.

- In the name of socialisation, parents who force their introverted kids to engage in constant “confidence-building” activities are actually causing a silent personality purge, substituting practiced extroversion for natural temperament, and raising a generation of adults who mistakenly associate psychological resilience love, and loyalty with chronic overcommitment and burnout.

- Psychology explains why the silent sacrifices made by parents in the 1960s and 1970s are now viewed as emotional neglect, even though their children refer to them as the source of their strength.

- This is the heartbreaking instance where a shelter shares a picture of an abandoned dog and the owner replies with a startling message.

- Sweden considers collaboration on nuclear weapons between France and Britain.

- A real living fossil: French scuba divers in Indonesian waters take the first, rare pictures of a species that is emblematic

- I cleaned my cabinets frequently, but I didn’t notice the grease that was concealed underneath.

March of these years? Why your retirement date might be reset in 2026

The main caution is that if you were born in March of the mid-1960s, the 2026 regulations may put you in the group of people whose State Pension age increases earlier than you anticipated. Not everyone is immediately affected by the increase to 67. March babies are right in the middle of it as it crawls month after month and year after year.

The precise day in March that you were born determines your State Pension date in addition to your year of birth. In the government schedule, two days apart can put you in different different bands entirely. Many people are caught off guard by that subtlety.

Consider Dave, who was born in March 1965 and works as a warehouse supervisor. He has worked nights, lifted, loaded, and been on his feet for forty years. He simply “knew for a” long time that he would receive his state pension at age 66 because his senior coworkers had informed him of this. He then received a link to the official calculator tool from his younger brother.

He didn’t realise the date on the screen was months later. More months of night work and sore knees. He had intended to work part-time and assist with his grandchildren for months, but those plans abruptly vanished. His expectations and reality had diverged due to a single, subtle change to the State Pension age schedule that would take effect in 2026.

The reasoning for this is ruthlessly straightforward. Different cohorts are subject to different regulations as the State Pension age is raised gradually. Individuals born in March frequently belong to transition groups, where the age ranges from 66 to 67 in small incremental steps.

When those rules change, no one alerts your phone with a siren or a flashing warning. You only get a sentence in a policy paper perhaps a paragraph on a news website.

To be honest, no one actually spends their Sunday lunch reading government consultation documents.

What to do right now if the 2026 increase could affect your March birthday

The first and most sensible step is to find out your precise State Pension age right now and stop speculating. Enter your birthdate into the official UK Government ‘Check your State Pension age’ tool, then note the precise day and year it displays. Next, take a moment to sit with that number.

Do this even if you “already know how” old you are if you were born in March of the 1960s. Memories alone are a dangerous guide because rules have changed so frequently.

Next, review your National Insurance history. Check your current number of qualifying years and the number you plan to accrue before the new pension age is implemented.

When they learn that their State Pension age is later, many people experience panic or rage. That is typical. After decades of following the rules, the finish line moves once more. Before you start making snap decisions, take a deep steady breath.

Assuming you have no control at all is the most frequent error. Although you cannot personally alter the pension schedule, you can alter your level of exposure to it. The impact of that additional working year can be mitigated by taking small tedious actions like completing gaps in your National Insurance record, beginning a small private pension, or increasing your savings rate by even £20 to £30 per month.

Another danger of denial is that if you ignore reality because it seems unfair, the date will still come.

According to one independent financial advisor I spoke with, “people don’t wake up one day and ‘suddenly’ hit State Pension age.” “What happens is that they make nebulous assumptions for twenty years, and when the letter comes, they realise they were wrong.”

- Use the official calculator to find out your exact State Pension age, particularly if you were born in March between the middle of the 1960s and the beginning of the 1970s.

- If there are any gaps in your National Insurance record that could lower your future pension, review it and think about making voluntary contributions.

- Investigate personal and workplace pensions to create a safety net so that the increase in the State Pension age does not completely determine when you can slow down.

- Discuss the implications of a later State Pension age for your joint plans honestly with your spouse or family.

- After 2026–2028 additional changes are being considered, so keep up with upcoming reviews of the State Pension age.

What this actually means for those born in March is that retirement is changing.

A straightforward, unsettling fact lies beneath all the graphs and policy discussions: the notion of a set predictable retirement age is eroding. The 2026 State Pension age changes serve as a stark reminder to those born in March of the “target years group” that the state’s promise may change during a working lifetime.

In response, some will try to work longer hours, some will reduce their hours earlier and rely more on personal savings, and some will modify their expectations regarding housing, travel, or assisting adult children. None of these answers are correct or incorrect. They are merely human attempts to take back control of a date that no longer belongs to them exclusively.

The reader’s value of the details

Growing age of the State PensionYou can determine whether you are in a “risk” group for a later pension date by moving toward 67 between 2026 and 2028, which most strongly affects specific March birth dates.

Verify your actual pension age.Instead of speculating or hearsay, use the official calculator and NI record.Avoid unpleasant surprises right before you want to end your workday.

Act quickly Close NI gaps, increase private savings, and discuss updated timelinesgives you more authority, even in the event that state regulations change frequently.

FAQ:

1. How can I determine whether my March birthday is impacted by the State Pension age increase in 2026?

Answer 1 Enter your complete date of birth using the government’s “Check your State Pension age” tool, then take note of the precise age and date provided. You are probably in or close to the cohorts impacted by the staged rise towards 67 if you were born in March during the mid-1960s to early 1970s.

Question 2: Will all March babies have to put in more time at work?

Response 2 No. The effect is contingent upon the year and day of your birth in March. Some people’s birthdays in March fall right before or right after a change. Because of this, two people who live just a few days apart may have different State Pension ages.

Question 3: If my State Pension age has increased, is there anything I can do?

Answer 3 Although you cannot reverse the legal change, you can lessen its effects. You can reduce your reliance on that one date by checking your National Insurance record, filling eligible gaps, increasing your personal or workplace pension savings, and making plans for part-time employment or phased retirement.

Question 4: What if I am unable to continue working until my new pension age due to health issues?

Answer 4 Depending on your situation, you might be eligible for certain benefits, occupational pensions, or ill-health provisions sooner. This is where individualised guidance—from a financial planner, union representative, or benefits adviser—becomes essential, particularly for people with physically demanding jobs.

Question 5: Should younger March-born individuals be concerned about increases after 2026?

Answer 5 Future reviews are already considering raising the State Pension age to 68. If you’re younger, start saving for retirement and use the State Pension basic safety net.